cross-posted from Cooperative Development Institute

Worker cooperatives can help build community wealth through sharing profits with workers. The Third Cooperative Principle is “Member Economic Participation” which describes how members invest into the cooperative and benefit from the surplus of the cooperative, as well as share any financial burdens it may have in difficult times. Similarly, the Second Cooperative Principle is Member Democratic Control, which is a key to this equitable sharing process as members decide how the surplus is distributed.

Your legal structure will determine different aspects of how the cooperative can distribute profit or surplus. For the sake of this blog post, I’m referring to Worker Cooperatives that are incorporated under corporate statutes. As incorporation statutes do change in different states, any of this information you would want to review with an accountant and/or lawyer in your state (and preferably one that knows co-ops – CDI can help you find one, get in touch.).

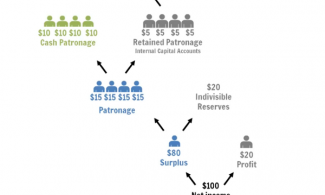

Cooperatives often define their profits as “surplus,” but more accurately surplus describes the net income that is generated by members, also known as worker-owners, whereas profit describes the net income that is generated by non-owner workers. For example, if you had a total of 1000 hours worked in the year with 600 hours worked by worker-owners and 400 hours worked by non-owner workers, then 60% of the total net income would be the “surplus” and 40% of the total net income would be the “profit.”

The profit generated by non-owner workers must be returned to the indivisible reserves of the cooperative and not distributed directly to the worker-owners. This helps to build the long-term capital of the cooperative and improves its financial stability.

The profit generated by non-owner workers must be returned to the indivisible reserves of the cooperative and not distributed directly to the worker-owners. This helps to build the long-term capital of the cooperative and improves its financial stability.

The ratio for the distribution of surplus is determined by the cooperative. Who determines this should be clearly defined in the bylaws. Some cooperatives leave it up to their board to decide each year how this is distributed, other cooperatives have defined ratios in their bylaws, while still others may decide on the ratio each year at their annual meeting of the worker-owners. Here’s where the principle of member democratic control is important, worker-owners need to have a democratic voice in how the surplus is distributed. Again this democratic process would be defined by the bylaws and could be made by consensus or majority vote, depending on the process of the cooperative.

Normally this ratio returns some money to the cooperative’s indivisible reserves (the co-op’s bank account, for instance) and then distributes some money to worker-owners through a combination of cash dividends and sometimes deposits in internal capital accounts. (Internal capital accounts are essentially accounts of revenue that the co-op holds onto, but belongs to worker-owners and accrues interest.) When there is a dividend, the law requires at least 20% be distributed directly to the worker-owner in cash so that the worker-owner can pay taxes on the dividend. Some worker-owned cooperatives return a larger percentage of their surplus into the cooperative’s indivisible reserves which can help the long term financial stability of the cooperative, while other cooperatives want to return more surplus to the worker-owners.

The remaining amount can be either distributed as cash or put into the worker-owners’ individual capital accounts. The capital accounts stay within the cooperative and can be drawn off, cashed out in a certain number of pre-determined years, or when a member leaves a cooperative.

Dividends to worker-owners are based on patronage. In a worker cooperative, patronage is based on the number of hours that a worker-owner worked in the past year. A common ratio that many worker cooperatives use to distribute is:

Dividend=$Total Surplus multiplied by Worker-Owners % of Total Hours

Individual Worker-Owners % of Total Hours= Total Individual Worker-Owner Hours in the Year divided by Total Hours by all Worker-Owners in the Year

While this is a common formula and dividends should be based on patronage, some co-ops may adjust this to include additional benefits for years worked at the co-op or retroactive compensation for hours worked by founders. It is important that this formula be approved by a democratic and transparent process.

Some worker cooperatives issue Class B or Preferred Shares. The bylaws would define when these shares could be issued, who can buy them, and how any dividend would be set. As a non-voting, passive equity investment option, Class B Shares offer an innovative way for co-ops to raise capital without ceding too much control. As the name implies, any dividends earned on Preferred Shares are paid before any distribution would be made to worker-owners.

Sharing profits is a great benefit of worker cooperatives, and when it is based on democratic principles it can lead to businesses that are more stable and equitable while also giving workers greater benefit from their labor.

Add new comment